It’s important that you know how to check your credit score for free. Your credit score is a critical piece of financial information that lenders, banks, and credit card companies use to evaluate your creditworthiness.

A good credit score can make it easier to get approved for loans and credit cards, and it can even help you secure better interest rates and loan terms. On the other hand, a bad credit score can make it difficult to qualify for credit or loans, and you may end up paying higher interest rates.

That’s why it’s essential to know your credit score and keep it in good standing.

In this article, we will guide you through the steps to check your credit score and understand what factors affect your credit score. We will also provide you with some tips and advice on how to improve your credit score.

Step 1 – Request Your Credit Report

The first step in finding out how to check your credit score for free is to request your credit report from one of the three major credit bureaus – Equifax, Experian, or TransUnion.

You can obtain your credit report for free of charge once every 12 months, as mandated by federal law. You can access your report online, by phone, or by mail.

Don’t be fooled by requests for payment or requests for other services or options.

Here are the steps to request your credit report:

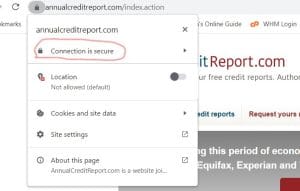

- Go to annualcreditreport.com, which is the only authorized website to provide free credit reports.

A word of warning!! You should never just click a link like this when preparing to submit personal information like your Social Security Number (SSN). Rather type the url into your browzer in a new window or tab.

Then check press “Enter” and check that the URL is the same as this one.

![]()

Click the “lock icon” in front of the URL to see if the connection is secure.

A message will appear saying that it is secure and then you can enter your private details.

If the website is not secure, do not under any circumstances enter your personal information, it is likely a scam.

Once you are happy that the website is legitimate, and you wish to receive your free credit report, follow the rest of the steps below;

- Select your state and click on “Request Report.”

- Enter your personal information, such as your name, date of birth, social security number, and current address.

- Select which credit bureau you want to receive your credit report from. You can choose to receive your credit report from all three credit bureaus at once or stagger them throughout the year.

- Answer a few security questions to verify your identity.

- Review your credit report and look for any errors or inaccuracies.

- If you find any errors, you can dispute them with the credit bureau.

Why is it important to review your credit report?

Reviewing your credit report is important because it provides a detailed account of your credit history.

It shows all the credit accounts you’ve opened and closed, your payment history, and any late payments or delinquent accounts. By reviewing your credit report, you can ensure that all the information is accurate and up-to-date.

If you find any errors or discrepancies, you can dispute them with the credit bureau to have them corrected.

How often should you check your credit report?

You should check your credit report at least once a year to make sure all the information is accurate.

However, if you’re planning to apply for credit or a loan in the near future, you should check your credit report at least three months in advance.

This will give you enough time to dispute any errors or inaccuracies before applying for credit.

Step 2 – Check Your Credit Report

Now that you have an idea of your credit score range, the next step is to get a copy of your credit report.

This report will give you a detailed breakdown of your credit history and the factors that influence your credit score.

- Request your credit report from the credit bureaus:

There are three major credit bureaus in the United States: Equifax, Experian, and TransUnion. Federal law requires that each of these bureaus provide you with a free copy of your credit report once a year. To obtain your report, you can visit annualcreditreport.com or call 1-877-322-8228.

- Review your credit report for errors:

Once you have your report, go through it thoroughly to check for errors. Mistakes on your credit report can harm your credit score, so make sure to look for any accounts that you don’t recognize or any incorrect information.

- Dispute any errors:

If you find any errors, you can dispute them with the credit bureau in question. You’ll need to provide documentation to support your claim, so make sure to keep copies of any relevant documents.

What if I Find Errors on My Credit Report?

If you find errors on your credit report, it’s important to take action to correct them. Dispute the errors with the credit bureau that is reporting them and provide any documentation to support your claim.

Once the credit bureau receives your dispute, they will investigate the claim and provide you with the results of their investigation.

If the credit bureau determines that the information is incorrect, they will remove it from your credit report. If they determine that the information is accurate, it will remain on your report. However, you can add a statement to your report explaining your side of the story.

What Should I Look for on My Credit Report?

When reviewing your credit report, make sure to look for the following:

- Incorrect personal information – Check that your name, address, and social security number are correct.

- Unauthorized accounts – Look for accounts that you don’t recognize.

- Incorrect account information – Make sure that the balances, payment history, and other account information is accurate.

- Inquiries – Check to see if there are any inquiries on your report that you didn’t authorize.

Check Your Credit Score With a Paid Service

Paid credit monitoring services offer comprehensive credit monitoring and alerts, as well as access to your credit reports and scores.

They typically charge a monthly or annual fee, but they can be worth it if you want to closely monitor your credit and receive timely alerts if there are any changes to your credit report.

If you suspect that you have been the subject of identity theft or some other online fraud, then a paid credit score service can save you from being liable for fraudulent debt.

To check your credit score with a paid service, follow these steps:

- Research and choose a reputable credit monitoring service that meets your needs.

- Sign up for the service and provide your personal and financial information as required.

- Once your account is set up, log in to your dashboard to view your credit report and score.

- Some services may also provide additional tools and resources to help you improve your credit score.

Step 3 – Monitor Your Credit Score and Report

Now that you have checked your credit score and report, it’s important to keep an eye on them going forward. Regular monitoring can help you catch errors early and take action to correct them.

Here are a few tips for monitoring your credit score and report:

- Sign up for credit monitoring – Many banks and credit card companies offer free credit monitoring services that alert you to any changes in your credit score or report.

- Set up fraud alerts – If you’re concerned about identity theft, you can set up fraud alerts with the credit bureaus. These alerts will notify you if someone tries to open an account in your name.

- Check your credit report regularly – You can request a free credit report from each of the three credit bureaus once a year. Consider requesting a report from a different bureau every four months to keep a closer eye on your credit.

What if My Credit Score Drops?

If you notice that your credit score has dropped, it’s important to investigate why. Review your credit report for any changes or errors and take action to correct them if necessary.

You can also work on improving your credit utilization ratio by paying down balances on your credit accounts.

Improving Your Credit Score

If your credit score isn’t as high as you’d like it to be, there are several steps you can take to improve it, including:

- Paying your bills on time – Payment history is the most important factor in your credit score, so make sure to pay all your bills on time to avoid late payments and potential delinquencies.

- Paying down debt – High credit utilization can negatively impact your credit score, so aim to keep your balances low and pay off any high-interest debt as soon as possible.

- Monitoring your credit report – Regularly checking your credit report can help you identify errors or inaccuracies that may be negatively impacting your score, as well as detect potential fraud or identity theft.

- Applying for credit sparingly – Opening too many new credit accounts at once can negatively impact your credit score, so be strategic about when and how often you apply for credit.

- Keeping old credit accounts open – The length of your credit history is also an important factor in your credit score, so avoid closing old credit accounts unless they have high fees or interest rates.

Further Explanation

There are many other resources available online for learning about credit scores and how to improve them. It’s important to do your research and make sure you’re using reputable sources of information.

Remember, your credit score is an important financial tool, and taking steps to improve it can have a significant impact on your financial future.

Final Thoughts

Checking your credit score is an important step in managing your finances and planning for your future. Whether you check your score for free or with a paid service, understanding how your score is calculated and how you can improve it can help you make better financial decisions and achieve your goals. By following the steps outlined in this guide, you can check your credit score and take control of your financial health.

Frequently Asked Questions About How to Check Your Credit Score for Free

Here are some frequently asked questions about checking your credit score:

1. How often should I check my credit score?

You should check your credit score at least once a year to make sure there are no errors or fraudulent activity on your credit report. You may also want to check your credit score more frequently if you’re planning to apply for credit or if you’re actively working to improve your credit.

2. Will checking my credit score hurt my credit?

No, checking your credit score will not hurt your credit. When you check your own credit score, it’s considered a “soft” inquiry and does not affect your credit score. However, when a lender or creditor checks your credit as part of a credit application, it’s considered a “hard” inquiry and may have a temporary negative impact on your credit score.

3. What factors affect my credit score?

Your credit score is based on several factors, including your payment history, credit utilization, length of credit history, types of credit used, and recent credit inquiries. Payment history and credit utilization are the two most important factors, so it’s important to pay your bills on time and keep your credit card balances low.

4. How can I improve my credit score?

There are several ways to improve your credit score, including paying your bills on time, paying down high credit card balances, avoiding new credit applications, and checking your credit report for errors and disputing any inaccuracies. It’s also important to maintain a mix of different types of credit, such as credit cards, loans, and a mortgage.

Additional Resources

If you want to learn more about credit scores and how to improve them, there are many great resources available online. Here are a few that we recommend:

AnnualCreditReport.com – This website is the only authorized source for free credit reports from the three major credit bureaus (Equifax, Experian, and TransUnion). You can request a free credit report once every 12 months.

Credit Karma – Credit Karma is a free website and app that provides credit scores and credit reports from two of the major credit bureaus (Equifax and TransUnion). It also offers personalized recommendations for improving your credit score.

MyFICO – MyFICO is a paid service that provides credit reports and credit scores from all three major credit bureaus, as well as credit monitoring and identity theft protection services.

The Credit Repair Organizations Act (CROA) – This federal law protects consumers from credit repair scams and regulates the credit repair industry. You can learn more about your rights and how to avoid scams by visiting the Federal Trade Commission’s website.

The National Foundation for Credit Counseling (NFCC) – The NFCC is a nonprofit organization that offers credit counseling, debt management programs, and other financial education services.